Manila Bulletin

Property and Living

Real estate market remains strong as effects of the Middle East crisis loom

Property and Living

Real estate market remains strong as effects of the Middle East crisis loom

Property and Living

Real estate market remains strong as effects of the Middle East crisis loom

Real estate market remains strong as effects of the Middle East crisis loom

According to Colliers Philippines, the year started positively for the property market, while challenges may come in the next quarters

Published May 18, 2026 09:52 am

Sail Residences will contribute 2,925 units in the Bay Area. (Artist's perspective: SMDC)

From its first-quarter property marketing briefing, Colliers Philippines reported that the real estate industry had a strong start in 2026. However, the positive performance posted flat growth, facing challenges from the Middle East crisis, with its impact expected in the next quarters.

According to Joey Roi Bondoc, Colliers Philippines research director, the year opened positively with 2,000 units net take-up, a 765 percent increase from 228 units recorded in the first quarter of 2025. "The Metro Manila residential sector showed early signs of recovery in the first quarter of 2026, driven by a sharp rebound in preselling activity and faster absorption of unsold inventory," said Bondoc. However, the projected net take-up for pre-selling is 8,000 units for 2026. The unsold ready-for-occupancy (RFO) is improving at 27,900 units of remaining inventory as of the first quarter of 2026, a slight decrease from 29,400 units in the same quarter last year.

In the last quarter of 2025, the net take-up came from the lower mid-income segment at 42 percent, the affordable segment at 15 percent, and the economic segment at 12 percent. Comparatively, in the first quarter of 2026, the net take-up was dominated by the affordable segment at 40 percent and the economic segment at 34 percent.

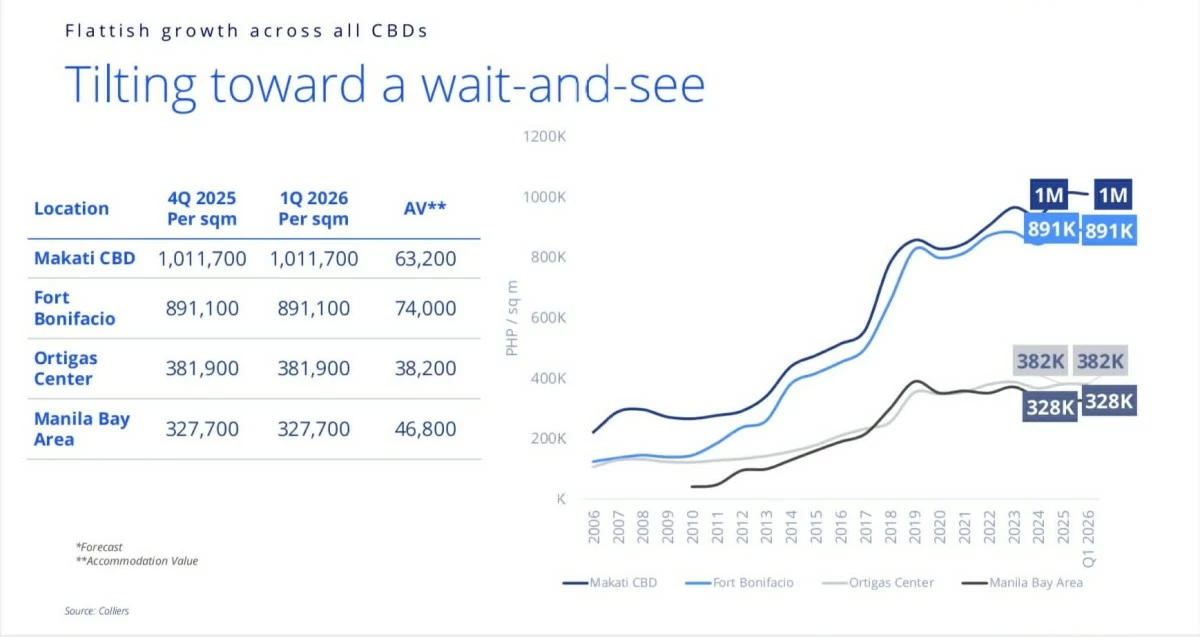

The property market registers flat growth pending the effects of the Middle East crisis. (Image: Colliers Philippines)

Bondoc pointed out a shift in which the affordable and economic segments gained a larger share of total units absorbed in Metro Manila, accounting for 74 percent. “This is a sharp increase from the 27 percent share in the two segments registered in the last quarter of 2025. This is because of the attractive and extended payment terms, very low down payment terms, and reservation fees that propelled those segments.”

He also mentioned the contribution of the Pambansang Pabahay Para sa Pilipino (4PH) program, which some developers are participating in, to bridge the 6.5 million housing gap. Some local government units have also launched their own housing development initiatives, such as Deparo Village and Banker’s Village in Caloocan, Urban Deca Homes in Tondo, and Sunny Ridge Residences in Mandaluyong.

The inventory life of the residential segment is now at its lowest, registered at 18 months. Meaning it will take 6.8 years for the market to fully absorb the unsold condo units in Metro Manila. The shorter inventory life points to an improving condo appetite.

For the first quarter this year, 2,000 new units were completed, including Cirrus Residences in C5 Corridor with 1,371 units, Aurelia Residences in Fort Bonifacio with 276 units, and Cerca Viento—Tower 3 in Alabang with 342 units.

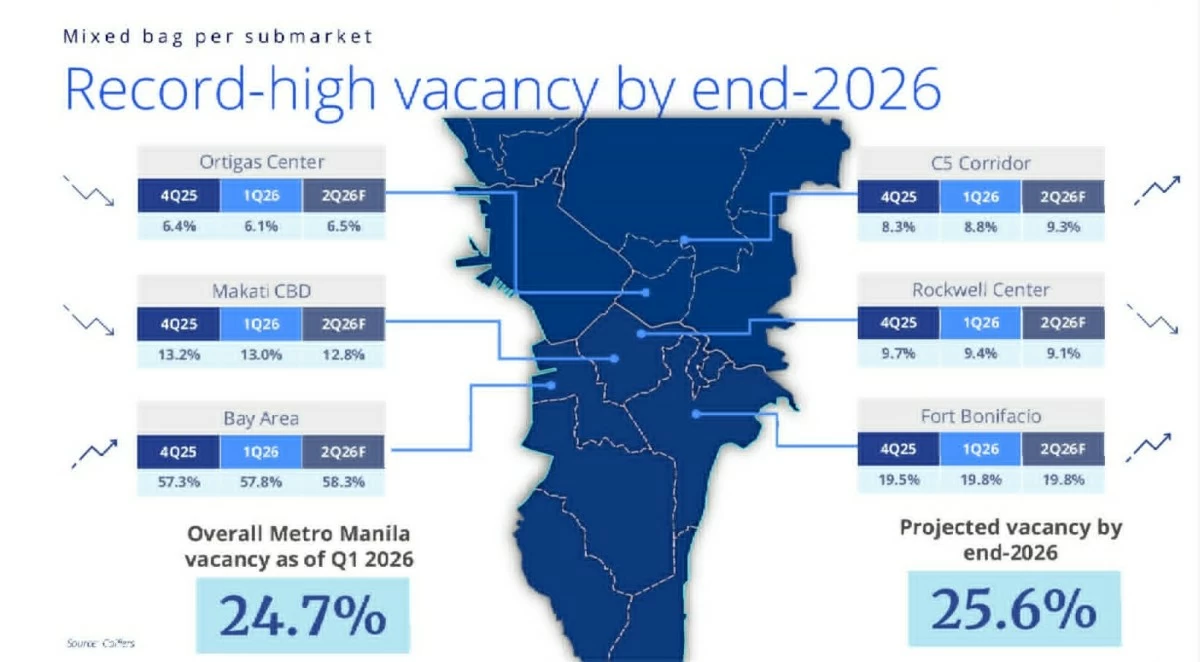

Metro Manila's vacancy rate remains high at 24.7 percent in the first quarter of 2026. (Image: Colliers Philippines)

A total of 12,900 units is scheduled to be completed by the end of 2026. The biggest supply contributors would be Sail Residences, with 2,925 units located in the Bay Area, and Gem Residences, with 1,452 units located in the C5 corridor, a fast-becoming residential hub.

The vacancy rate in the residential secondary market now stands at 24.7 percent and will likely reach 25.6 percent by year-end. The Bay Area vacancy rate remains the highest at 59.4 percent and will likely remain elevated until year-end.

Office Services - Tenant Representation Director Kevin Jara reported that the office sector has sustained its transaction activity, as well as held a steady vacancy rate of 19 percent across Metro Manila submarkets in the first quarter of 2026. He also forecasted a 400,000 sqm net take-up for 2026 despite the ongoing crisis.

The office demand held steady at 193,000, a 13 percent decrease based on year-on-year data but a 12 percent increase from the last quarter.

Most of the transactions came from the traditional segment at 113,000 sqm, third-party operations at 41,000 sqm, shared services at 22,000 sqm, and government at 17,000 sqm. Surprisingly, there was a growth in shared services of 122 percent compared to year-on-year data.

Fort Bonifacio remains the most active market, with transactions involving 40,000 sqm, followed by Makati with 38,000 sqm, Alabang with 34,000 sqm, and the Bay Area at 22,000 sqm.

A total of 500,000 sqm of office space is scheduled to be completed this year and another 200,000 sqm in 2027. Colliers also noted minimal to no upcoming PEZA-accredited stock in primary markets such as Makati, Ortigas, and BGC. A 1.46 million sqm PEZA space is still available in Metro Manila, with 44 percent being aging units.

Arca South Integrated Terminal, the transport-oriented development in Taguig (Artist's perspective: Ayala Land)

Provincial transactions dropped to 32 percent, with 37,000 sqm in transactions recorded from the first quarter of 2026 versus 55,000 sqm in the same quarter of 2025. Some major provinces, however, have shown improvements in vacancy rates, such as Davao leading at 7 percent, Metro Cebu at 16 percent, and Pampanga at 20 percent.

Transit-oriented developments are on the rise with upcoming transport hubs, such as Grand Central Station and ARCA South Integrated Terminal, both scheduled to be completed in 2027, and the Metro Manila Subway Project in 2032.

In the retail sector, Bondoc said that mall developers and retailers are heading towards premiumization in Metro Manila and outside the National Capital Region, the next phase of retail. Small retail formats have also proliferated, with The Plaza Bagong Silang at 2,000 sqm, Park Triangle Mall at 9,000 sqm, and The Shoppes at Park McKinley West at 13,000 sqm.

As of the first quarter of 2026, the retail vacancy recorded at 10.8 percent and is expected to be at 10.2 percent by the end of the year. There is a total of 7.9 million sqm of leasable space in Metro Manila, with an additional 96,000 sqm of new retail space in the first quarter of 2026.

From 2026 to 2028, major retail developments include the completion of Ayala Malls Parklinks, SM Harrison, and Filinvest Mall Cubao, the expansion of Fisher Mall and SM Fairview, and the redevelopment of SM Megamall, Robinsons Forum Mall, and Greenbelt 1 and 2. An estimated annual average of 113,000 sqm of new retail supply will be produced for the same period.