Business

Intensified US-China trade tensions may weaken Philippine peso—Oxford Economics

Business

Intensified US-China trade tensions may weaken Philippine peso—Oxford Economics

Intensified US-China trade tensions may weaken Philippine peso—Oxford Economics

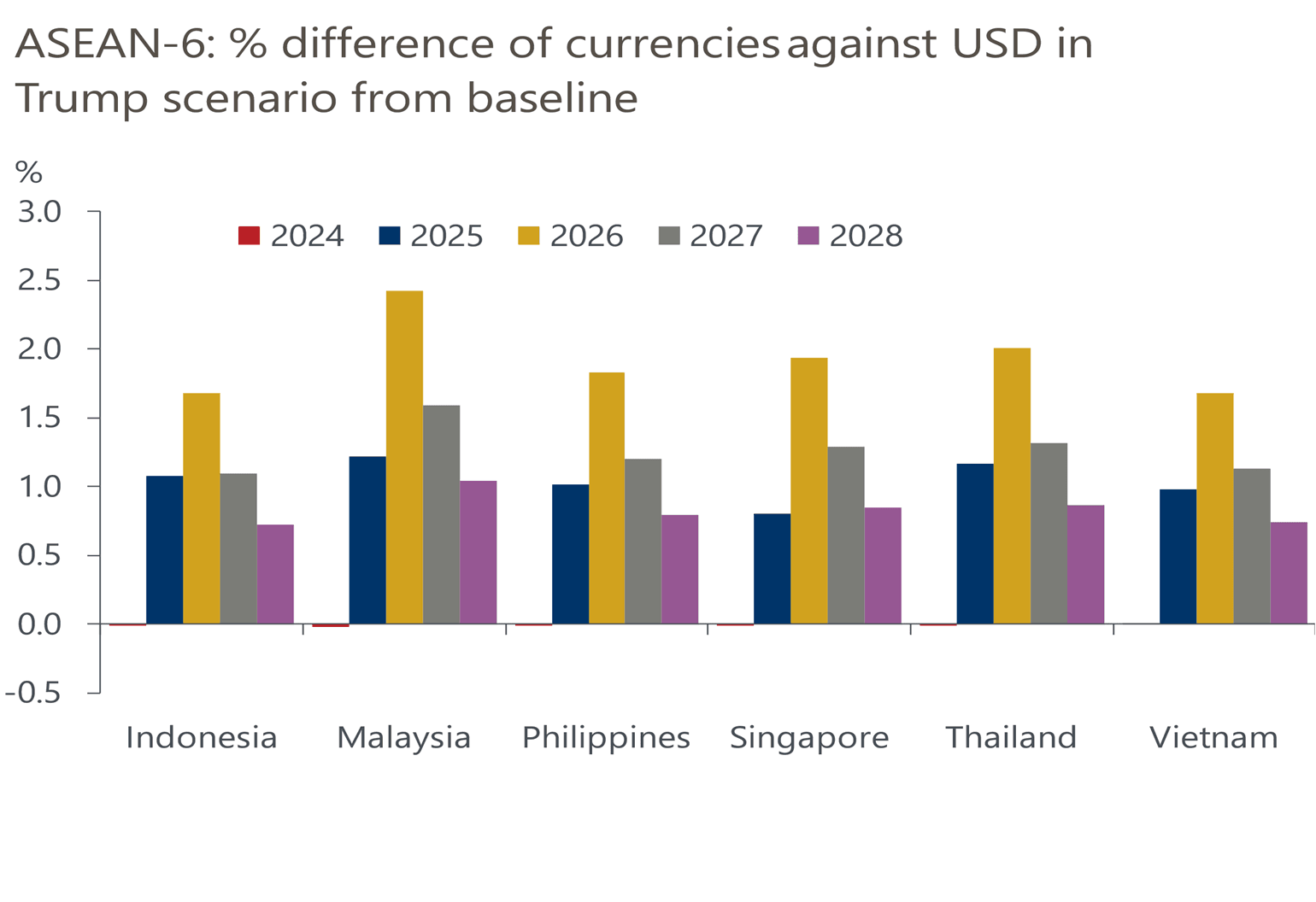

An intensified trade war between the United States and China in case Donald J. Trump retakes the US presidency may weaken currencies in the Association of Southeast Asian Nations (ASEAN), especially the Philippine peso, according to the think tank Oxford Economics.

In a report on Monday, Sept. 23, Oxford Economics assistant economist Adam Ahmad Samdin pointed out that if the US further jacks up import tariffs slapped against Chinese goods under another Trump presidency, a weakening in ASEAN currencies would spill over to their central banks' respective monetary policy decisions.

"The main reason for a stronger US dollar is the US Federal Reserve keeping rates higher than the baseline forecast, due to higher inflation rates... (mainly) from higher imported inflation from higher US tariffs," Samdin explained.

As imports to the US would become more expensive due to additional duties on these products, Samdin said the resulting strengthening of the greenback would weigh on currencies in the region.

Under a "Trump scenario,” Oxford Economics expects volatile currencies in ASEAN-6, which includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam, especially by 2026, when their depreciation is expected to be most pronounced against the US dollar.

"These movements are relevant for monetary policy in ASEAN, as some central banks watch for currency stability. Within the region, central banks in Indonesia and the Philippines are at the highest risk of cutting rates more slowly and having a higher terminal rate. Other ASEAN economies will be affected, but to a lesser extent," Samdin said.

"Policy rates in Indonesia and the Philippines are more sensitive to US rates and dollar movements due to structural current account deficits and open capital accounts. Even if other ASEAN currencies depreciate more against the US dollar, we think these central banks will be more sensitive since there's less of a buffer," Samdin noted.

"Reduced monetary headspace compared to the baseline could be an issue during a domestic slowdown," Samdin added.

Samdin said that "tariffs will not only affect exports in the near term, but the Fed's reaction to higher US inflation will also impact ASEAN economies."

In ASEAN-6, the Philippines has the biggest deficit in the current account or net dollar earnings, equivalent to 4.6 percent of gross domestic product (GDP).

Last week, the Bangko Sentral ng Pilipinas (BSP) projected a larger end-2024 current account deficit of $6.8 billion than the earlier estimate of $4.7 billion. Also, the updated estimated deficit of $5.5 billion for 2025 was nearly triple the previous BSP projection of $2 billion.

The yawning current account deficit would be brought about by expectations of slower growth in goods and services exports as well as business process outsourcing (BPO) revenues, according to the BSP.

As the Philippines is a net importer of the goods it consumes, the country spends more dollars to buy products overseas, resulting in the current account deficit putting pressure on the peso.